Part of our Global Banking Surveillance Series | Read the UK investigation →

Commonwealth Bank’s Carbon Tracker: The Full Story

Your reader is correct that Commonwealth Bank has been tracking carbon footprints for over two years. Here’s the complete timeline and current status.

NatWest Carbon Tracker and UK Digital ID: Separating Fact from Fiction

When It Started

Commonwealth Bank launched its carbon footprint tracker in October 2021 as a pilot program with 250,000 customers, then rolled it out to all retail customers in August 2022. This makes it approximately 3+ years that the feature has been available, not just “over 2 years” as your reader mentioned.

How It Works

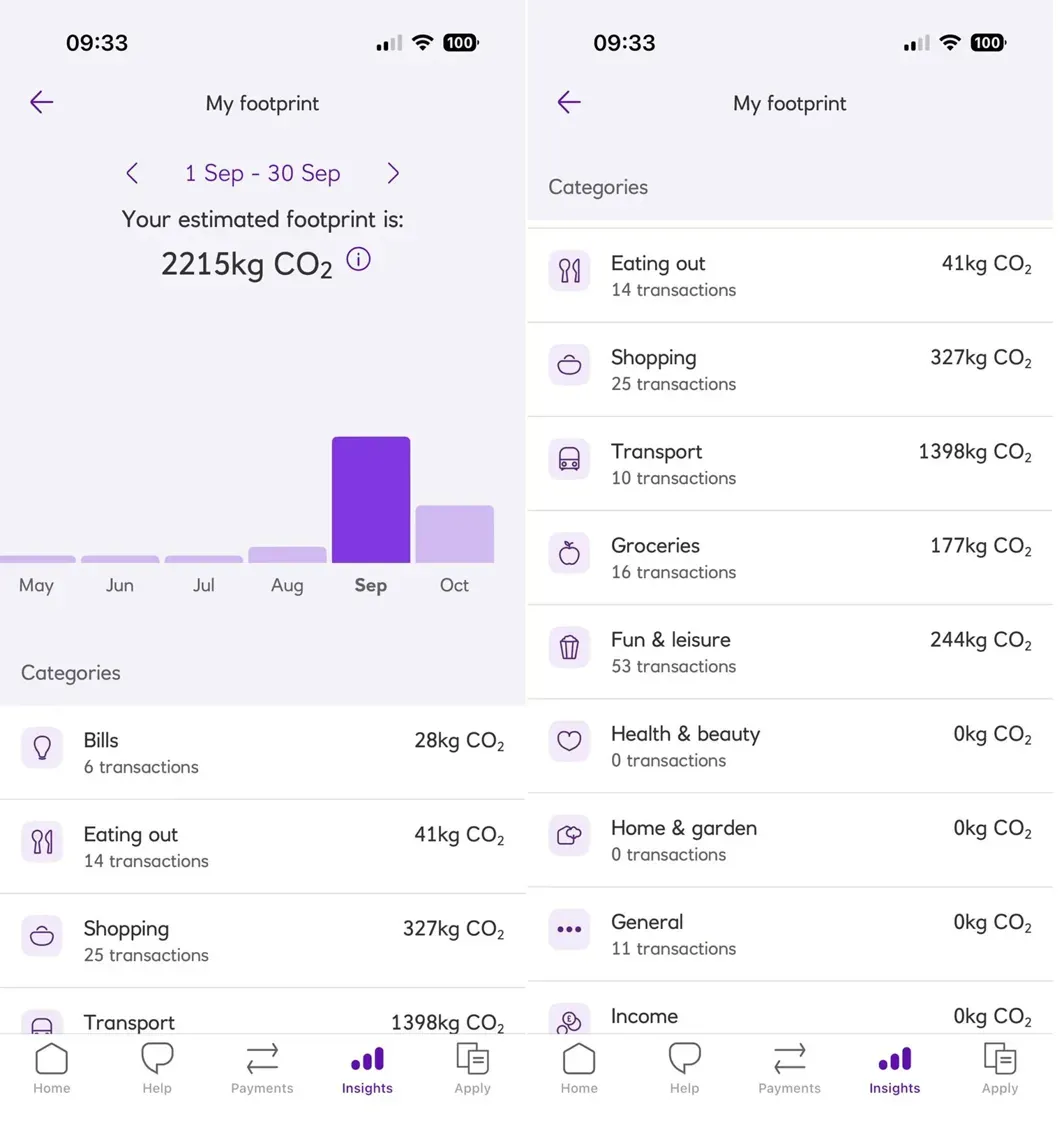

The tracker analyzes transactions from customers’ Everyday accounts, credit cards, and BPAY, assigning emission factors to each purchase based on industry category (fashion, grocery, transport, etc.). The technology was developed through a partnership with Cogo, the same New Zealand fintech company that powers NatWest’s UK carbon tracker.

Customers can view their monthly carbon footprint compared to the national average, with breakdowns by categories like Utilities, Transportation, and Shopping.

If you have the combank app, they’re already tracking your carbon footprint.

That’s why I only use cash in person. pic.twitter.com/zLfGtE29Zz— The People’s King Elvis (@Real_King_Elvis) December 13, 2023

The Critical Question: Was It Removed?

Important Clarification: Based on current evidence, the carbon tracker has NOT been removed from the CommBank app.

As of late 2024/early 2025:

- CommBank’s website still hosts multiple pages about carbon tracking and “Carbon Insights”- The feature is referenced in their current sustainability materials- No official announcement of its removal has been made

However, it’s possible that:

- The feature may be less prominently displayed in recent app updates2. Some customers may not see it if they don’t have eligible accounts3. The interface may have changed, making it harder to find

Opt-In or Automatic? The Controversy

This is where things get murky and concerning. Some reports from 2022 stated that “all customers now automatically opting in to the initiative”, which would be significantly different from NatWest’s explicitly optional approach.

However, we need to note:

- Official CommBank statements emphasize customer choice and providing “options”- No official documentation clearly states it’s mandatory- The exact opt-in/opt-out process remains unclear in public materials

This lack of transparency is troubling and deserves scrutiny. If customers were indeed “automatically opted in,” this represents a significant difference from the UK approach and raises legitimate privacy concerns.

”Covert Tracking” Claims

The claim that “most banks have been doing it covertly” requires examination:

What’s True:

- All banks analyze transaction data for various purposes (fraud detection, credit scoring, marketing)- Banks can technically calculate carbon footprints from transaction data without showing it to customers- The infrastructure to track this data exists even if the feature isn’t visible

What’s Speculation:

- No evidence suggests banks are secretly tracking carbon footprints without customer knowledge- If tracking occurs for carbon calculations, it would typically only be for customers using the visible tracker feature- Claims of “covert” tracking without evidence can be misleading

The Real Concern: Even if tracking isn’t “covert,” the question of whether customers were automatically enrolled without explicit consent is a legitimate privacy issue that deserves answers.

Carbon Tracking in Financial Services: Compliance, Privacy, and Digital Identity Convergence

Westpac’s Carbon Tracker

Westpac launched its own carbon footprint tracker in May 2023, also partnering with Cogo. The feature works similarly to CommBank’s:

- Estimates carbon emissions from spending on eligible accounts- Provides comparisons to Australian individual and household averages- Links to educational resources about sustainable living

Like CommBank, questions about opt-in vs. automatic enrollment remain unclear in public documentation.

What About ANZ and NAB?

Based on research, ANZ and NAB do not appear to offer customer-facing carbon footprint trackers as of October 2025. Both banks:

- Have made institutional climate commitments- Track their own operational and financed emissions- Have not announced consumer carbon tracking features similar to CommBank or Westpac

The Elephant in the Room: Banking Hypocrisy

Here’s where the story gets truly interesting and deeply hypocritical. While these banks are tracking your carbon footprint from buying groceries or taking the bus, let’s examine their own environmental records:

Fossil Fuel Financing

In 2023, Australia’s big four banks (ANZ, NAB, CommBank, and Westpac) loaned $3.6 billion to fossil fuels, including $2.5 billion to companies expanding coal, oil, and gas.

Breaking it down by bank:

NAB (the biggest fossil fuel lender in 2023):

- $1.4 billion to fossil fuels in 2023, including $860 million to companies with coal, oil, and gas expansion plans

ANZ (Australia’s biggest funder of fossils since Paris Agreement):

- Nearly $1 billion to companies developing new coal, oil, and gas in 2023- More than $20 billion to fossil fuels since the Paris Agreement was signed

Westpac:

- $784 million to fossil fuels in 2023, with over $533 million to companies expanding fossil fuels

Commonwealth Bank:

- $271 million to fossil fuels in 2023 (the least of the big four)

The Context

Leading experts, including the International Energy Agency and the Intergovernmental Panel on Climate Change, agree: achieving the Paris Agreement’s climate goals requires no new coal, oil, or gas development.

Yet these same banks that want to help you “understand your carbon impact” from buying a dress or eating meat are simultaneously pouring billions into the companies most responsible for climate change.

The “Greenwashing” Accusation

Critics argue that carbon tracking features represent a form of greenwashing, given that banks like Commonwealth Bank remain heavy financiers of fossil fuels, having poured tens of billions into companies expanding the fossil fuel industry.

Ask yourself:

- Why should you worry about the 16kg of CO₂ from buying a dress when your bank just funded a coal mine expansion?- Who bears more responsibility for climate change: individual consumers or the financial institutions enabling fossil fuel expansion?- Is this about genuine environmental concern or shifting blame from corporations to individuals?

Digital ID Connection in Australia?

Unlike the UK, there is no evidence of plans to connect carbon tracking to digital ID systems in Australia. However, that doesn’t mean it couldn’t happen in the future, which is why vigilance and clear privacy laws are essential.

Australia’s Digital ID Infrastructure: A Reality Check

While carbon trackers and digital IDs aren’t connected yet, Australia is building comprehensive digital surveillance infrastructure that makes such integration technically possible. Here’s what’s actually happening:

Australia’s Digital ID Act 2024

As documented in our comprehensive analysis, Australia’s Digital Revolution: Age Verification and ID Checks Transform Internet Use, Australia has implemented:

- Digital ID Act 2024 (commenced December 1, 2024)- Mandatory age verification for search engines (started December 27, 2025)- Under-16 social media ban requiring ID checks for all users- Nationwide Digital ID system for accessing government and business services

The Reality of Australia’s Age Verification System

The Australian government has admitted what privacy advocates warned about: to enforce the under-16 social media ban, every single user—regardless of age—will need to upload government ID. This means:

- The government can track every social media post- Every comment, every like, every interaction becomes traceable- VPNs won’t protect users’ privacy- A comprehensive database of online activity will be created

Seven Methods of Age Verification:

- Photo ID uploads (driver’s license, passport)2. Facial recognition and biometric scans3. Credit card verification4. Digital ID through accredited services5. AI inference from behavioral patterns6. Document verification7. Third-party verification services

The AU10TIX Connection: Israeli Surveillance Tech in Australia

What makes Australia’s system particularly concerning is its use of AU10TIX, an Israeli identity verification company, for processing government IDs. This raises questions about:

- Data sovereignty (Australian ID data processed offshore)- Foreign government access to Australian citizens’ information- Security of centralized biometric databases- Lack of transparency in data handling

Global Digital Surveillance: The Bigger Picture

Australia’s system is part of a coordinated global push for digital identity and surveillance. As we’ve documented in The Global Digital Crackdown: How Governments and Corporations Are Dismantling Online Freedom in 2025, similar systems are being implemented worldwide:

United Kingdom:

- Mandatory “Brit Card” digital ID for employment- Age verification requiring government ID- Full analysis of UK’s digital ID system

Mexico:

- Mandatory biometric ID including iris scans and fingerprints- Required from birth to death- How Mexico created the Western Hemisphere’s most comprehensive surveillance system

Russia:

- State-linked digital ID embedded in mandatory Max app- Integration with government services and commerce- Russia’s surveillance system copying China’s model

European Union:

- Continent-wide age verification and digital identity systems- Cross-border surveillance infrastructure- How Europe is implementing mass surveillance under the guise of safety

Understanding Different Digital ID Models

For those interested in the technical and policy differences between systems, see our Policy Briefing: The Global Digital Identity Landscape, which analyzes:

- Centralized vs. federated models- Government vs. private sector approaches- Biometric vs. non-biometric systems- Privacy protections and oversight mechanisms

The Convergence Threat

While carbon tracking and digital ID aren’t connected now, the infrastructure exists for integration. Consider how these systems could converge:

Today (Separate Systems):

- Banks track your carbon footprint from purchases- Government tracks your identity via Digital ID- Platforms track your online activity via age verification- Financial institutions track transactions for AML/KYC

Tomorrow (Integrated Systems):

- Your Digital ID links to your bank account- Your carbon footprint affects your credit score- Your online activity influences insurance rates- Your financial access depends on behavioral compliance- Social credit system emerges without ever being explicitly created

Why This Matters: The Chinese Model

Australia’s trajectory raises uncomfortable parallels to China’s social credit system. As detailed in our analysis The End of Digital Privacy: How Global Digital ID, CBDCs, and State Surveillance Are Reshaping Human Freedom, we’re seeing:

Components Being Built:

- Digital ID systems (authentication)2. CBDC development (financial control)3. Online surveillance laws (behavior monitoring)4. Age verification (identity linkage)5. Carbon tracking (consumption monitoring)

What Integration Could Enable:

- Real-time monitoring of all financial transactions- Linking online speech to real-world identity- Financial exclusion based on behavior or beliefs- Automated enforcement of social norms- Pre-emptive restrictions on “undesirable” activities

The Privacy Erosion Playbook

Across all these systems, governments follow a similar pattern:

Step 1: Introduce with noble justification

- “Protect the children”- “Stop illegal immigration”- “Fight climate change”- “Prevent money laundering”

Step 2: Implement gradually

- Start with pilot programs- Begin with “voluntary” adoption- Make opt-out complicated or impossible

Step 3: Expand scope creep

- Add more required use cases- Lower age requirements- Extend to more services- Share data across systems

Step 4: Normalize surveillance

- Present as inevitable technological progress- Dismiss privacy concerns as paranoid- Point to other countries doing the same- Make non-participation socially costly

Step 5: Make reversal impossible

- Integrate into critical infrastructure- Create dependency on the system- Eliminate alternatives- Establish legal requirements

What Makes Australia’s Situation Unique

Australia’s approach is particularly aggressive compared to other Western democracies:

Speed of Implementation:

- Digital ID Act and social media ban within months- Mandatory age verification rolled out rapidly- Limited public consultation or debate

Scope of Coverage:

- Affects all citizens, not just specific groups- Covers both online and offline activities- No realistic opt-out provisions

Foreign Technology:

- Reliance on Israeli verification company AU10TIX- Data processing potentially occurring offshore- Lack of transparency about data handling

Weak Privacy Protections:

- Limited oversight mechanisms- Unclear data retention policies- Insufficient penalties for misuse

Digital ID Connection in Australia?

Comparison: Australia vs. UK

Feature UK (NatWest) Australia (CBA/Westpac)

Launch Date November 2021 October 2021 (CBA), May 2023 (Westpac)

Technology Partner Cogo Cogo

Explicitly Optional? Yes - Must opt-in Unclear - Claims of automatic enrollment

Can Customers Opt Out? Yes - Clear instructions provided Unknown - No public documentation

Transparency Relatively high Relatively low

Bank’s Fossil Fuel Funding 38.6% government owned Billions in fossil fuel loans annually

What Should Customers Do?

If You’re a Commonwealth Bank Customer:

- Check your app - Open your CommBank app and look for “Carbon Insights” or similar features in your spending section2. Look for settings - Search for carbon tracking in your app settings3. Contact the bank - Call CommBank and explicitly ask:

- Is carbon tracking active on my account?- Was I automatically opted in?- How do I opt out?4. Document everything - Keep records of any interactions about this feature

If You’re a Westpac Customer:

Follow the same steps as above, looking for carbon footprint or sustainability features in your app.

General Privacy Steps:

- Review app permissions - Check what data your banking apps can access2. Read terms and conditions updates - Banks often introduce new features via ToS updates3. Use privacy settings - Opt out of any data sharing that isn’t essential for basic banking4. Consider alternatives - If transparency concerns you, research smaller banks and credit unions with clearer privacy practices

The Bigger Picture

The carbon tracking story reveals several important truths:

1. Individual vs. Corporate Responsibility

Banks tracking your carbon footprint while funding fossil fuel expansion represents a fundamental misdirection. Major financial institutions pushing consumer carbon awareness while continuing to invest heavily in environmentally hazardous projects raises serious questions about priorities and accountability.

2. Data Privacy in the Digital Age

Whether carbon tracking is “covert” or not, the fact that banks can and do analyze granular transaction data for various purposes should concern anyone who values privacy. The question isn’t just “are they tracking my carbon footprint?” but “what else are they doing with my transaction data?“

3. The Transparency Problem

The lack of clear, accessible information about opt-in/opt-out processes for carbon tracking reflects a broader problem in banking: features get added, terms of service update, and customers are expected to navigate complex privacy settings without clear guidance.

4. The Climate Hypocrisy

Perhaps the most galling aspect is banks positioning themselves as climate leaders by helping customers track grocery store emissions while simultaneously financing the fossil fuel industry. It’s a masterclass in corporate greenwashing.

Key Questions That Remain Unanswered

- **Were CommBank customers automatically enrolled in carbon tracking without explicit consent?**2. **Can customers easily opt out, and if so, how?**3. **What data is retained even after opting out?**4. **Is the feature genuinely “removed” or just relocated in app updates?**5. **What safeguards exist against carbon tracking data being used for other purposes in the future?**6. Will carbon footprint data affect credit decisions, insurance, or other financial services?

What Needs to Happen

For carbon tracking programs to be ethical and legitimate, banks must:

- Make enrollment explicitly opt-in - No automatic enrollment2. Provide clear opt-out processes - Easy to find and execute3. Ensure data transparency - Customers should know exactly what’s tracked and how it’s used4. Commit to data limitations - Carbon data should never be used for credit scoring, insurance, or other discriminatory purposes5. Address their own carbon footprints - Stop funding fossil fuel expansion before lecturing customers about sustainability6. Be honest about impact - Individual carbon footprints pale in comparison to corporate and industrial emissions

Examples of Resistance and Alternatives

Not all digital ID implementations face passive acceptance. Some examples of pushback:

UK Public Resistance: Over 2.76 million people signed a petition against the Brit Card digital ID. While the government has dismissed these concerns, the level of opposition demonstrates public awareness of the risks. Read about the GOV.UK ID Check App controversy.

Decentralized Platforms Fighting Back: When Mississippi passed an age verification law, decentralized platforms like Mastodon demonstrated how federated architecture can resist state control. The Decentralized Resistance story shows alternatives exist.

Technical Countermeasures: Services like NextDNS have introduced features to bypass age verification requirements, using DNS-level geo-spoofing. Learn about the DNS revolution against digital ID laws.

Switzerland’s Democratic Approach: In 2021, Swiss voters rejected a government-backed digital ID system in a referendum, showing how direct democracy can check surveillance expansion when citizens are empowered to decide.

Australia Compared to Other Models

Australia’s approach differs significantly from other implementations:

Country System Mandatory Biometric Privacy Protections

Australia Centralized Yes (for many services) Yes (via AU10TIX) Weak

UK Centralized Yes (employment) Yes Moderate

Mexico Centralized Yes (universal) Yes (iris & fingerprint) Very Weak

Estonia Federated Optional No Strong

Switzerland Rejected N/A N/A Citizens voted against

For detailed analysis of different digital ID models worldwide, see our comprehensive guide: Digital IDs and Personal Privacy: Navigating the Benefits and Risks.

🎧 Related Podcast Episode

Conclusion

Yes, Commonwealth Bank has been tracking carbon footprints for over three years, and Westpac has been doing it since 2023. The feature does not appear to have been completely “removed,” though its visibility and accessibility may have changed.

The Three-Layer Problem:

Layer 1: The Carbon Tracking Issue

- Lack of transparency about opt-in processes- Questionable automatic enrollment (if true)- Unclear opt-out mechanisms- Unknown data retention and usage

Layer 2: The Banking Hypocrisy

- Banks tracking your grocery emissions while funding fossil fuels- $3.6 billion loaned to fossil fuel expansion in 2023 alone- Individual blame while enabling corporate polluters- Greenwashing through sustainability features

Layer 3: The Digital Surveillance Infrastructure

- Mandatory Digital ID system (December 2024)- Age verification requiring government ID for all users- Biometric data collection via AU10TIX- No current connection to carbon tracking—but infrastructure exists

Why the Australian Situation is Particularly Concerning:

Australia has become a test case for how quickly and comprehensively a Western democracy can implement digital surveillance:

- Speed: Multiple systems launched within months2. Scope: Covers social media, search engines, banking, government services3. Mandatory nature: Limited opt-out options4. Foreign tech: Israeli verification company handling Australian data5. Weak oversight: Limited independent review or accountability

The Global Context:

Australia isn’t alone. As documented in The Global Digital Crackdown, similar systems are being implemented globally:

- UK’s Brit Card and age verification- Mexico’s mandatory biometric ID- Russia’s state-linked Max app- EU’s continent-wide digital identity system

For comprehensive analysis of these systems, see:

- Global Digital ID Systems Status Report 2025- Policy Briefing: The Global Digital Identity Landscape

What Australians Should Do:

Immediate Actions:

- Contact Your Bank

- Explicitly ask if carbon tracking is active- Request details on opt-in/opt-out procedures- Ask about data retention and sharing policies- Document all responses2. Know Your Digital Rights

- Understand what the Digital ID Act requires- Know what data is collected during age verification- Review your rights under Australian Privacy Principles3. Protect Your Privacy

- Use privacy-respecting services when possible- Minimize data shared with financial institutions- Consider smaller banks or credit unions with better privacy practices- Use VPNs and privacy tools (while still legal)

Long-Term Advocacy:

- Demand Transparency

- From banks about carbon tracking enrollment- From government about Digital ID data usage- About AU10TIX and offshore data processing2. Support Legislative Change

- Strong privacy protections in law- Independent oversight of surveillance systems- Data minimization requirements- Interoperability restrictions3. Build Community Resistance

- Connect with privacy advocacy groups- Support platforms and services that prioritize privacy- Share information about surveillance expansion- Participate in public consultations4. Follow the Money

- Pressure banks to stop fossil fuel financing- Support financial institutions with genuine climate commitments- Question the hypocrisy of carbon tracking + fossil funding

The Bigger Picture:

The convergence of carbon tracking, digital ID, age verification, and financial monitoring creates infrastructure for comprehensive surveillance. Whether this infrastructure is used for benign purposes or transforms into something more sinister depends on:

- Public Awareness: Understanding what’s being built2. Democratic Oversight: Demanding accountability3. Legal Protections: Strong privacy laws with teeth4. Technical Alternatives: Supporting privacy-preserving systems5. Corporate Resistance: Banks and tech companies refusing overreach

Why This Matters Globally:

Australia is being watched by governments worldwide. If comprehensive digital surveillance can be rapidly implemented in a Western democracy with minimal resistance, it provides a blueprint for others to follow. That’s why the stakes are so high.

The Choice Before Us:

We can accept the narrative that surveillance is inevitable technological progress, that privacy is outdated, and that convenience justifies any intrusion. Or we can insist that democratic societies require:

- Privacy as a fundamental right- Transparent governance- Meaningful consent- Limited government power- Independent oversight

The infrastructure is being built. The question is whether we’ll set boundaries before it’s too late.

Research conducted October 2025 based on official bank statements, news reports, and financial analysis from multiple sources including Market Forces, Cogo, and Australian financial media.

Additional Resources

Privacy and Digital Rights:

- MyPrivacy.blog - Comprehensive digital privacy coverage- ComplianceHub.wiki - Policy and regulatory analysis- Australian Privacy Principles (APPs) - Your rights regarding personal data

Banking and Finance:

- Market Forces: Tracking Australian bank fossil fuel financing- Cogo: Understanding carbon tracking technology

Essential Reading:

- Australia’s Digital Revolution: Age Verification and ID Checks- The End of Digital Privacy: How Global Digital ID, CBDCs, and State Surveillance Are Reshaping Human Freedom- Digital IDs and Personal Privacy: Navigating the Benefits and Risks

Stay vigilant. Demand transparency. Protect your rights.